import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

from datetime import datetime,timedelta

from time import time

数据读取与预处理

cat_fish = pd.read_csv('./data/catfish.csv',parse_dates=[0],index_col=0,squeeze=True)

cat_fish.head()

Date

1986-01-01 9034

1986-02-01 9596

1986-03-01 10558

1986-04-01 9002

1986-05-01 9239

Name: Total, dtype: int64

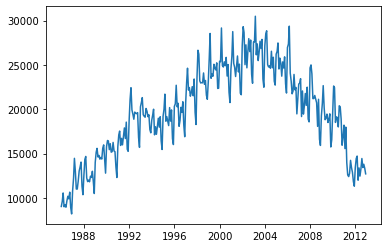

时序图

plt.plot(cat_fish)

[<matplotlib.lines.Line2D at 0x16f1ea95bb0>]

序列有明显的趋势性

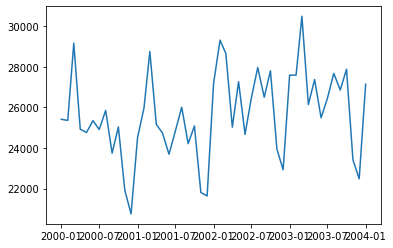

start = datetime(2000,1,1)

end = datetime(2004,1,1)

plt.plot(cat_fish[start:end])

[<matplotlib.lines.Line2D at 0x16f1f8b7fa0>]

有很明显周期性

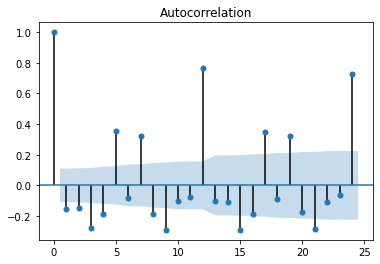

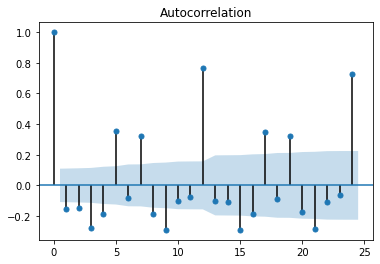

自相关系数图

from statsmodels.graphics.tsaplots import plot_acf,plot_pacf

plot_acf(cat_fish.diff(1)[1:],lags=24)

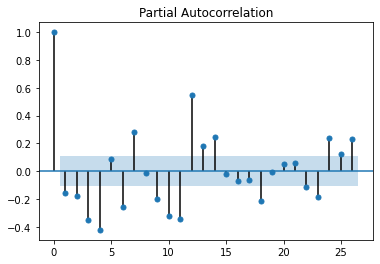

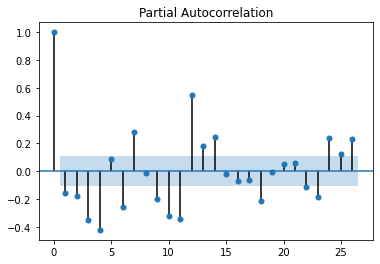

偏自相关系数图

plot_pacf(cat_fish.diff(1)[1:])

偏自相关系数图12步差分时,相关系数比较大,剔除趋势性后,原始数据还是呈现出明显的周期性

白噪声检验

from statsmodels.stats.diagnostic import acorr_ljungbox

acorr_ljungbox(cat_fish.diff(1)[1:],lags=[6,12,18,24],return_df=True)

|

lb_stat |

lb_pvalue |

| 6 |

95.719733 |

1.957855e-18 |

| 12 |

373.541488 |

1.498233e-72 |

| 18 |

466.300398 |

1.243989e-87 |

| 24 |

731.756632 |

5.126647e-139 |

不是白噪声

使用SARIMA(0,1,0)x(1,0,1,12)进行预测

(0,1,0)是一阶差分,提取趋势性信息

(1,0,1,12)是ARMA(1,1),季节周期为12,提取季节性信息

模型训练

from statsmodels.tsa.statespace.sarimax import SARIMAX

print(cat_fish.index[0],cat_fish.index[-1])

1986-01-01 00:00:00 2012-12-01 00:00:00

train_end = datetime(2009,1,1)

test_end = datetime(2010,1,1)

train_data = cat_fish[:train_end]

test_data = cat_fish[train_end + timedelta(days=1):test_end]

model = SARIMAX(train_data,order=(0,1,0),seasonal_order=(1,0,1,12))

model_fit = model.fit()

model_fit.summary()

C:\Users\lipan\anaconda3\lib\site-packages\statsmodels\tsa\base\tsa_model.py:159: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

warnings.warn('No frequency information was'

C:\Users\lipan\anaconda3\lib\site-packages\statsmodels\tsa\base\tsa_model.py:159: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

warnings.warn('No frequency information was'

SARIMAX Results

| Dep. Variable: |

Total |

No. Observations: |

277 |

| Model: |

SARIMAX(0, 1, 0)x(1, 0, [1], 12) |

Log Likelihood |

-2296.563 |

| Date: |

Sat, 03 Apr 2021 |

AIC |

4599.126 |

| Time: |

17:13:59 |

BIC |

4609.988 |

| Sample: |

01-01-1986 |

HQIC |

4603.485 |

|

- 01-01-2009 |

|

|

| Covariance Type: |

opg |

|

|

|

coef |

std err |

z |

P>|z| |

[0.025 |

0.975] |

| ar.S.L12 |

0.9889 |

0.007 |

135.425 |

0.000 |

0.975 |

1.003 |

| ma.S.L12 |

-0.7923 |

0.054 |

-14.692 |

0.000 |

-0.898 |

-0.687 |

| sigma2 |

9.069e+05 |

7.77e+04 |

11.666 |

0.000 |

7.55e+05 |

1.06e+06 |

| Ljung-Box (Q): |

71.38 |

Jarque-Bera (JB): |

0.57 |

| Prob(Q): |

0.00 |

Prob(JB): |

0.75 |

| Heteroskedasticity (H): |

2.47 |

Skew: |

0.08 |

| Prob(H) (two-sided): |

0.00 |

Kurtosis: |

3.16 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

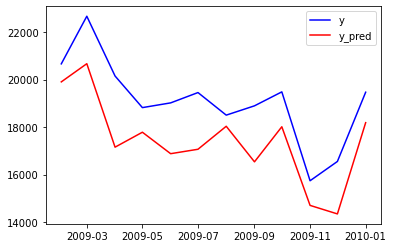

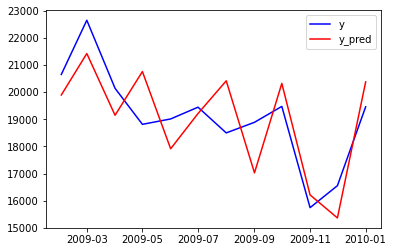

预测

predictions = model_fit.forecast(len(test_data))

predictions = pd.Series(predictions,index=test_data.index)

residuals = test_data - predictions

plt.plot(test_data,color ='b',label = 'y')

plt.plot(predictions,color='r',label='y_pred')

plt.legend()

plt.show()

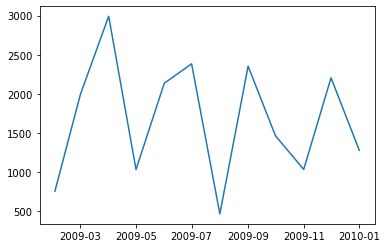

残差图

plt.plot(residuals)

[<matplotlib.lines.Line2D at 0x16f35389c40>]

残差白噪声检验

acorr_ljungbox(residuals,lags=10,return_df=True)

|

lb_stat |

lb_pvalue |

| 1 |

2.974643 |

0.084579 |

| 2 |

3.702085 |

0.157073 |

| 3 |

9.938764 |

0.019094 |

| 4 |

16.441791 |

0.002480 |

| 5 |

16.607813 |

0.005307 |

| 6 |

17.906828 |

0.006469 |

| 7 |

21.149384 |

0.003555 |

| 8 |

21.996374 |

0.004923 |

| 9 |

22.067707 |

0.008667 |

| 10 |

22.789588 |

0.011550 |

循环预测

predictions_new = test_data.copy()

for train_end in test_data.index:

train_data = cat_fish[:train_end-timedelta(days = 1)]

model = model = SARIMAX(train_data,order=(0,1,0),seasonal_order=(1,0,1,12),freq='MS')

model_fit = model.fit()

pred = model_fit.forecast(1)

predictions_new[train_end] = pred

plt.plot(test_data,color ='b',label = 'y')

plt.plot(predictions_new,color='r',label='y_pred')

plt.legend()

plt.show()

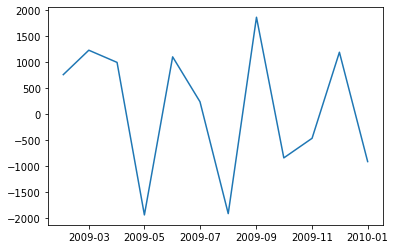

plt.plot(test_data-predictions_new)

[<matplotlib.lines.Line2D at 0x16f3878bdc0>]

print('RMSE:', np.sqrt(np.mean(residuals**2)))

RMSE: 1832.9537663585463

residuals_new = test_data-predictions_new

print('RMSE:', np.sqrt(np.mean(residuals_new**2)))

RMSE: 1242.0409950292837