对于量化交易来说,量化策略和技术系统缺一不可,为了知其所以然,本文实现了一个C++连接CTP接口进行仿真交易的demo,从接收行情、下订单、数据处理到添加策略、挂载运行交易等多个环节来看一下量化交易的最简单流程,管中窥豹,一探究竟。

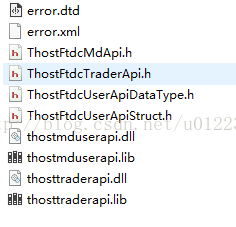

这里使用上期所提供的CTP接口API,通过CTP可以连接交易所进行行情接收交易。下载地址:CTP下载

本文使用的win32版本的,linux版本用法类似。

CTP接口包含以下内容:

整个开发包有2个核心头文件包括4个核心接口,

CThostFtdcMdApi接口和CThostFtdcTraderApi两个头文件,一个处理行情,一个处理交易。

(1)处理行情的CThostFtdcMdApi接口有两个类,分别是CThostFtdcMdApi和CThostFtdcMdSpi,以Api结尾的是用来下命令的,以Spi结尾的是用来响应命令的回调。

(2)处理交易的CThostFtdcTraderApi接口也有两个类,分别是CThostFtdcTraderApi和CThostFtdcTraderSpi, 通过CThostFtdcTraderApi向CTP发送操作请求,通过CThostFtdcTraderSpi接收CTP的操作响应。

要连接期货交易所交易,需要开设自己的账户,实现期货交易、银期转账、保证金等功能,由于小白一般不会用实盘资金交易,所以此处推荐用上期所提供的simnow虚拟交易平台simnow申请一个虚拟账户。

SIMNOW提供两类数据前置地址:

(1)交易时段的地址,如09:00-15:00和21:00-02:30,使用第一套地址,这些数据是真实的行情数据,只是时间上比真实的行情会有延迟30秒左右(SIMNOW从交易所接收后转发出来的)。

(2)非交易时段地址,这时的数据是历史行情的播放,比如昨天的数据之类的,可以用来做程序调试。

建议选择申请那个7x24行情的账户,便于开发调试。

其中,

一个简单的程序化交易系统需要完成的业务可以划分为:

1.基本操作,比如登录,订阅等;

2.行情操作,比如对行情数据的接收,存储等

3.订单操作,比如报单;对报单,成交状况的查询;报单,成交状况的私有回报等。

4.数据监听和处理操作,比如接收到新数据之后的统计处理,满足统计条件后的报单处理(其实这里就是我们的策略所在)

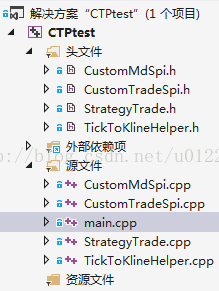

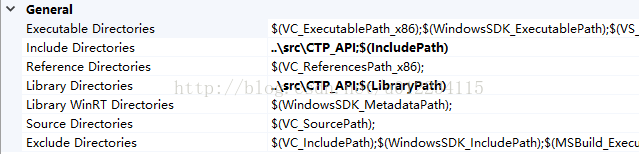

visual studio创建工程后,首先需要将ctp的头文件以及链接库(lib和dll)目录配置到工程

连接到交易所,需要配置经纪商代码、帐户名、密码以及订阅合约和买卖合约的相关参数

这里只是简单的写一下,真实完整的交易系统中,一般用配置文件,有用户去定制

继承CThostFtdcMdSpi实现自己的行情回调类CustomMdSpi,在系统运行时这些重写的函数会被CTP的系统api回调从而实现个性化行情

CustomMdSpi头文件

都是重写回调函数

连接应答

登录应答

订阅行情应答

深度行情通知

同理,也需要继承CThostFtdcTraderSpi来实现自己的CustomTradeSpi类,用于交易下单、报单等操作的回调

CustomTradeSpi头文件

除了重写的基类函数,还自己封装一些主动调用的操作函数,比如登入登出、下单报单、查询报单等

登录应答

查询投资者结算结果应答

查询合约应答

查询投资者资金帐户应答

查询投资者持仓应答

这里把下单录入的操作放在了持仓结果出来之后的回调里面,策略交易也简单的放在了这里,真实的情况下,应该是由行情触发某个策略条件开一个线程进行策略交易

下单操作

通过重载写了两个函数,一个是用默认参数下单,一个可以传参下单,比如设定合约代码、价格、数量等

报单操作

主要是对于未成交的订单进行编辑或者撤销操作

报单应答

等待成交进行轮询可以选择报单操作,成交完成后的应答

从交易拿到的tick数据是时间序列数据,在证券交易中其实还需要根据时间序列算出一些技术指标数据,例如MACD,KDJ、K线等,这里简单地对数据做一下处理,写一个TickToKlineHelper将时间序列专程K线

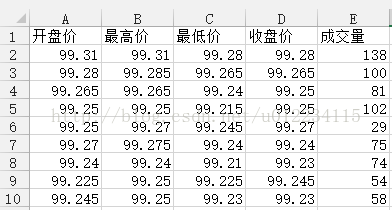

K线数据结构

转换函数

量化交易系统最终是需要将编写的策略代码挂载到系统中进行策略交易的,这里做了一个简单的实现

StrategyTrade.h

StrategyTrade.cpp

main.cpp

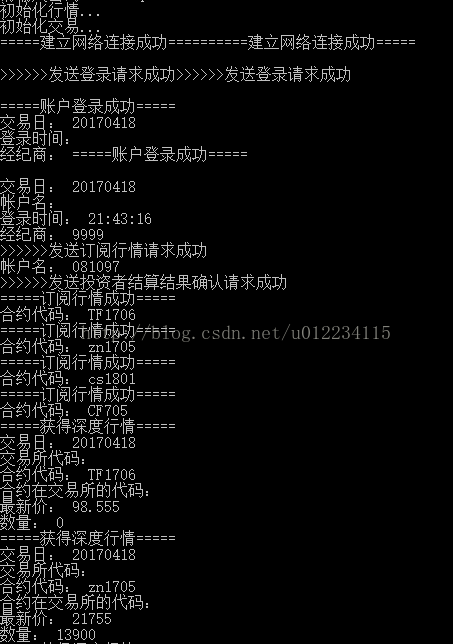

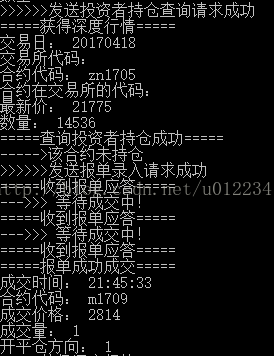

应答日志

存成csv表格

应答日志

用上期所的快期软件,登录上自己的账号之后,从过程序下单,在这个界面里能看到实时的报单成交状况

csdn:demo

github:demo

本文旨在为刚接触CTP的小白们抛砖引玉,各交易接口的深度运用还需要看官方开发文档。

另外,对于完整的量化交易系统来说,不仅要具备行情、交易、策略模块,事件驱动、风控、回测模块以及底层的数据存储、网络并发都是需要深入钻研的方面,金融工程的Quant Researcher可以只专注于数据的分析、策略的研发,但是对于程序员Quant Developer来说,如何设计和开发一个高并发、低延迟、功能完善与策略结合紧密的量化交易系统的确是一项需要不断完善的工程。

ps:如果需要更高级和细致甚至可以用于实盘的功能,比如完整的开源交易系统,数据系统,算法交易,数据和交易接口等完备的解决方案,由于博客回复不现实,只能私信联系啦~