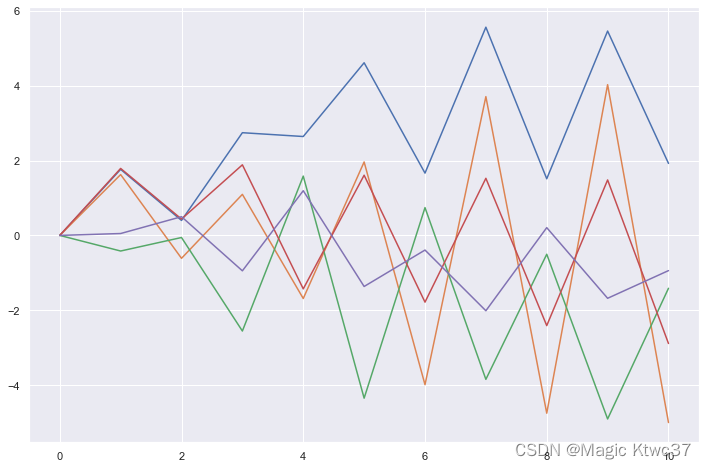

蒙特卡洛模拟通常被用来对不同结果的概率建模,这些结果因为一些相关的随机因素而难以预测。蒙特卡洛模拟的构建方法千差万别,但它们一般会根据一个假设的概率分布来生成随机的输入,然后根据这些输入来计算或者聚合出结果。简单来说,蒙特卡洛模拟就是至少运行模型上千次,得到一系列的结果,这些结果会呈现一个概率分布,后结合所有结果来组成一个概况。 蒙特卡洛模拟的应用非常广,尤其是在金融领域,例如期权定价模型(Black Scholes Model)、违约风险分析(在线价值,Value at Risk)等。 蒙特卡洛模拟的简单模型应是单根或者随机步行模型。随机步行模型通过变量历史值加上一个随机噪声来得到当前的结果,该随机噪声通常被定义为是一个标准正态分布。请见下式:

S

t

=

S

t

−

1

+

Z

t

,

S

0

=

0

,

Z

t

∼

N

(

0

,

1

)

S_t=S_{t-1}+Z_t,S_0=0,Z_t \sim N(0,1)

St=St−1+Zt,S0=0,Zt∼N(0,1)

随机步行

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

%matplotlib inline

sns.set()

monte_carlo =[]for i inrange(5):

forecasts =[0]

np.random.seed(i)for j inrange(10):

forecast = forecasts[j-1]+ np.random.normal()

forecasts.append(forecast)

monte_carlo.append(forecasts)

plt.figure(figsize=(12,8))

plt.plot(np.array(monte_carlo).T);

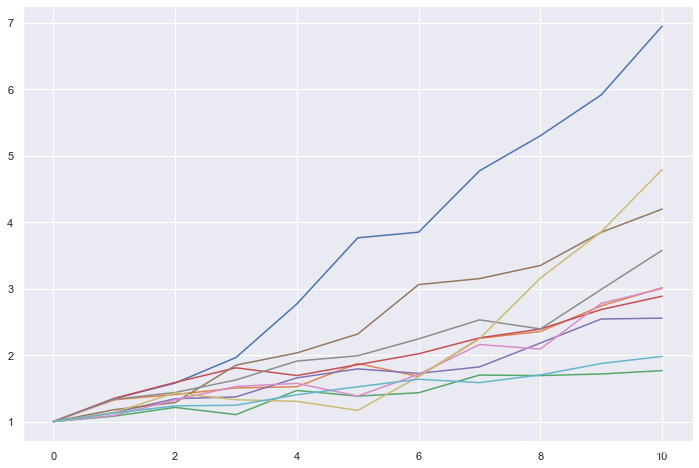

GBM模型公式如下:

S

t

=

S

0

e

x

p

(

(

μ

−

σ

2

/

2

)

t

−

σ

×

W

t

)

S_t=S_0exp((\mu-\sigma^2/2)t-\sigma\times W_t)

St=S0exp((μ−σ2/2)t−σ×Wt)

W

t

−

W

t

−

1

=

d

t

Z

t

W_t-W_{t-1}=\sqrt{dt}Z_t

Wt−Wt−1=dtZt

Z

t

∼

N

(

0

,

1

)

Z_t\sim N(0,1)

Zt∼N(0,1)

这里,

μ

\mu

μ为偏移率,确定了随机过程平均值的变化,

σ

\sigma

σ是该变化的波动。 GBM模型亦可以写成如下形式:

S

t

=

s

t

−

1

e

x

p

(

(

μ

−

σ

2

/

2

)

d

t

−

σ

d

t

Z

t

)

S_t=s_{t-1}exp((\mu-\sigma^2/2)dt-\sigma \sqrt{dt}Z_t)

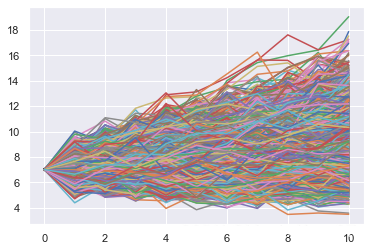

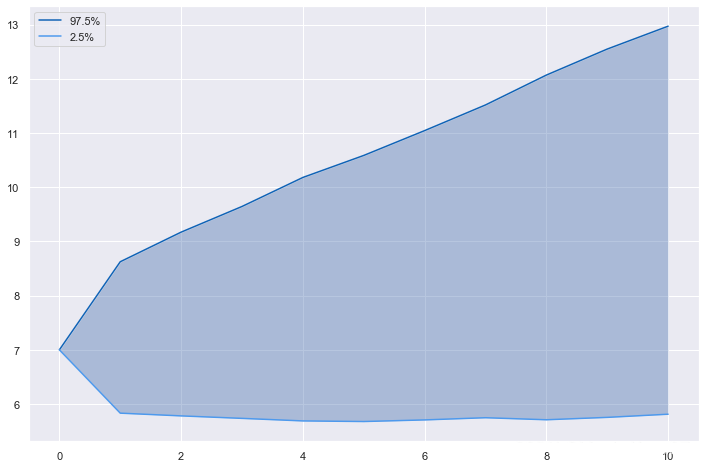

St=st−1exp((μ−σ2/2)dt−σdtZt) 下图展示了GBM模型的10个模拟,参数为:

S

0

=

1

,

μ

=

0.05

,

σ

=

0.2

S_0=1,\mu=0.05,\sigma=0.2

S0=1,μ=0.05,σ=0.2

monte_carlo =[]

no_of_iter =10

sigma =0.2

mu =0.5

delta_t =0.25for i inrange(no_of_iter):

np.random.seed(i)

forecasts =[1]for j inrange(10):

forecast = forecasts[j]*np.exp((mu-sigma**2/2)*(delta_t)+ sigma*np.sqrt(delta_t)*np.random.normal())

forecasts.append(forecast)

monte_carlo.append(forecasts)

x = np.array(monte_carlo)

plt.figure(figsize=(12,8))

plt.plot(x.T);

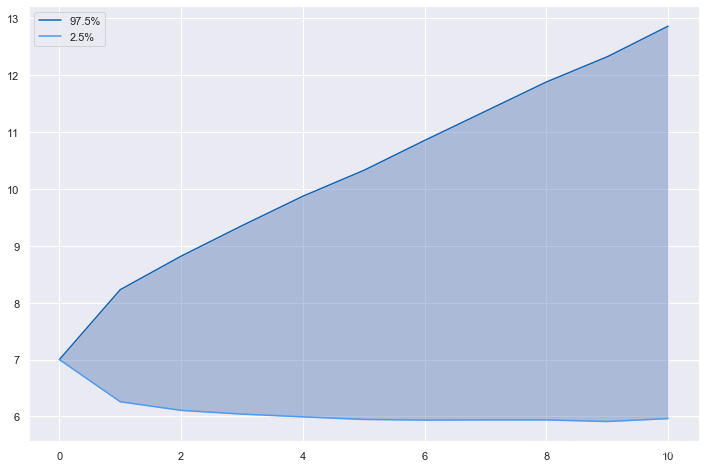

金融预测应用蒙特卡洛模拟

我们先建立一个简单的金融模型,

P

r

o

f

i

t

=

R

e

v

e

n

u

e

−

F

i

x

e

d

C

o

s

t

−

V

a

r

i

a

b

l

e

C

o

s

t

Profit=Revenue-FixedCost-VariableCost

Profit=Revenue−FixedCost−VariableCost